Cost Comparison: Rent vs. Buy

Depending on individual finances, investing in a home may result in lower monthly costs than renting. Several variables determine the costs of a home loan, explained Eric Kilstrom, senior vice president of V.I.P. Mortgage, serving Anthem, all of Arizona and 21 other states:

- Lenders determine interest rates based on your credit score and the ratio of the loan amount to the home’s value.

- Credit scores below 640 will rarely qualify for conventional loans.

- A down payment of less than 20 percent on a conventional loan may require private mortgage insurance (PMI). PMI protects the lender if the owner defaults.

- The lowest down payment typically allowed on a conventional loan is 3 percent, but PMI will tend to be higher.

- FHA loans, backed by the federal government and aimed at low- to moderate-income borrowers, have looser credit standards and allow modest down payments but always have PMI.

- VA loans for service members and veterans, also backed by the government, never have PMI but carry a related fee instead.

Borrowers can lower interest rates by paying “points” up front, which can make sense if interest rates are high and a buyer plans to stay in a home for a long time.

“With interest rates as low as they are now, it doesn’t make much sense for most people to pay points, unless they’re dealing with poor credit,” Kilstrom said.

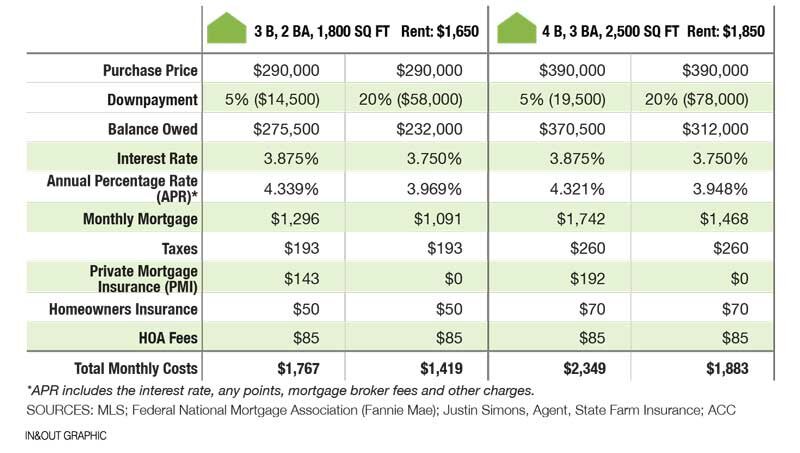

Monthly Home Ownership vs. Rental Costs

Estimated costs of renting either of two typical single-family homes in Anthem Parkside versus buying, assuming a credit score of 720 and a 30-year fixed-rate mortgage:

See Also: Columnist Chris Prickett weighs in on other factors in the rent vs. buy equation.

See Also: Columnist Chris Prickett weighs in on other factors in the rent vs. buy equation.